A measurement-first proposal for Wave · timed to the business-Trends rollout

Eliciting merchant cashflow beliefs at Wave, and using them to design the cash-advance product

Wave's cash-advance product deducts a share of each incoming customer payment until the advance plus a flat fee is repaid. Because repayment scales with revenue, merchants' beliefs about their own future cashflows — Wave revenue, off-Wave revenue, expenses, fees — are the central determinant of who takes the product, how it performs, and which terms fit which merchants. We propose a phased collaboration that begins by measuring those beliefs and uses what we learn to design the cash-advance trial. The business-Trends rollout in Senegal and Côte d'Ivoire then provides a natural setting for a dashboard RCT (Phase 3) that tests how merchant-facing data presentation moves forecast calibration, fee perception, and downstream business outcomes.

The proposal in one paragraph ¶

─── three phases · measurement informs the cash-advance trial · dashboard RCT timed to the rollout

Phase 1 — Measure merchant cashflow beliefs. A 3–5 minute phone or in-app belief-elicitation module covering: next-month Wave revenue forecast (Bloom-style, accuracy-bonused), expected non-Wave revenue over the same window, one expense category (Augenblick-style category-cued retrieval), perceived fees paid last month (Wave charges 1% above 20,000 F/day; the open question is how merchants perceive that), a gross-margin estimate, a counterfactual cash-advance use-case + expected incremental return, and stated valuation of bundled platform features. Beliefs are verified against Wave's server-side records. Deliverables to Wave inside 1–3 months: calibrated merchant beliefs at the firm and sector level; a sector-margin slice on deduction burden; a direct number on the gap between perceived and actual fees; willingness-to-pay for sticky platform add-ons. Detail in §02.

Phase 2 — A cash-advance trial designed from the Phase 1 evidence. Wave's cash advance is live in The Gambia (10% deduction per incoming customer payment, 10% flat fee, automatic repayment, no compounding or late fees). Six concrete product variations — loan-size formula, pre-filled loan suggestion, deduction-rate cadence, fee-disclosure framing, state-contingent deduction around predictable expense spikes, and a hybrid debt-fixed contract — each correspond to a belief pattern Phase 1 will identify or rule out. The Phase 1 evidence picks which to vary in Phase 2 rather than forcing the choice ex ante. Phase 2 runs on a separate Gambia sample and does not require Phase 1 to be written up first. Detail in §03.

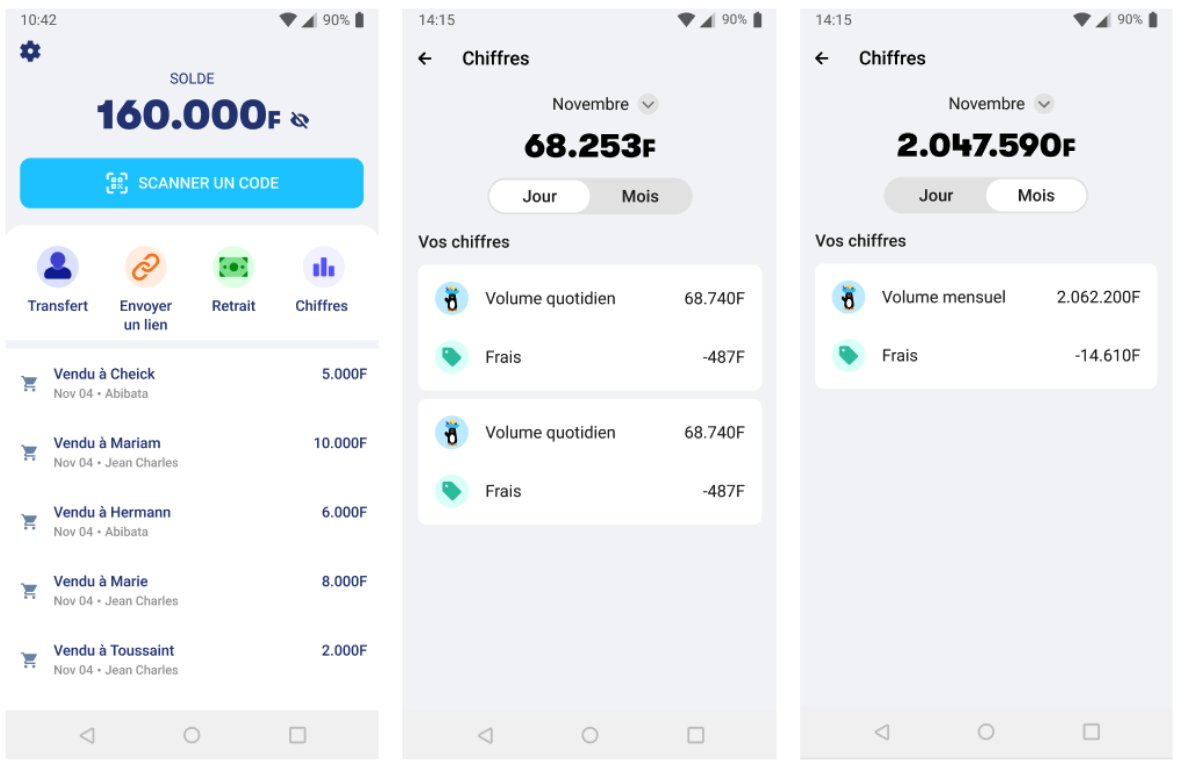

Phase 3 (optional) — A dashboard RCT timed to the business-Trends rollout. The business-Trends product ("Chiffres") is in pre-launch in Senegal and Côte d'Ivoire — currently shows Volume + Frais without a category breakdown. Phase 3 evaluates the rollout itself with a 2×2 (engagement nudges × content) cross-randomized with a fee-display sub-arm, with a no-contact control and a per-category opt-out welfare guardrail. This is the publishable Trends paper — it answers whether the dashboard's category breakdown causally moves merchant outcomes and whether engagement nudges sustain that effect after removal. Phase 3 is optional from Wave's side; Phase 1 and Phase 2 stand independently. Detail in the §05 appendix.

The fee-perception measurement in Phase 1 directly addresses Colin's hypothesis that small merchants over-estimate the fees they pay — currently a strategic open question for Wave's pricing and product communication. Phase 2's six cash-advance variations give Robert Grande's team a structured menu of pre-registered tests rather than ad-hoc product tweaks. And Phase 3 lets Wave evaluate the business-Trends rollout itself — the closest precedents (Bar-Gill et al. 2024 on eBay's Seller Hub +3.6% in weekly sales, Gertler et al. 2025 on Mexican Clip merchants +15% adoption from reminders) suggest meaningful causally-identified effects on merchant outcomes are achievable in this setting.

Phase 1 · Measurement ¶

─── 3–5 minute belief module · revenue · expenses · fees · cash-advance items

Wave already has the best half of the measurement: every transaction flows through Wave's rails, so revenue, fees paid, cash-advance utilization, repayment, and engagement are server-side and ground-truthed. What's missing is the belief side — how merchants expect their own next-month revenue, expenses, and fees to look. We fill that gap with a single 3–5 minute phone or in-app module. The module can be delivered in 1–3 months on a sample of 600–1,200 merchants and does not require the business-Trends rollout to be live first.

A Bloom-style revenue forecast, asked of treatment and control merchants

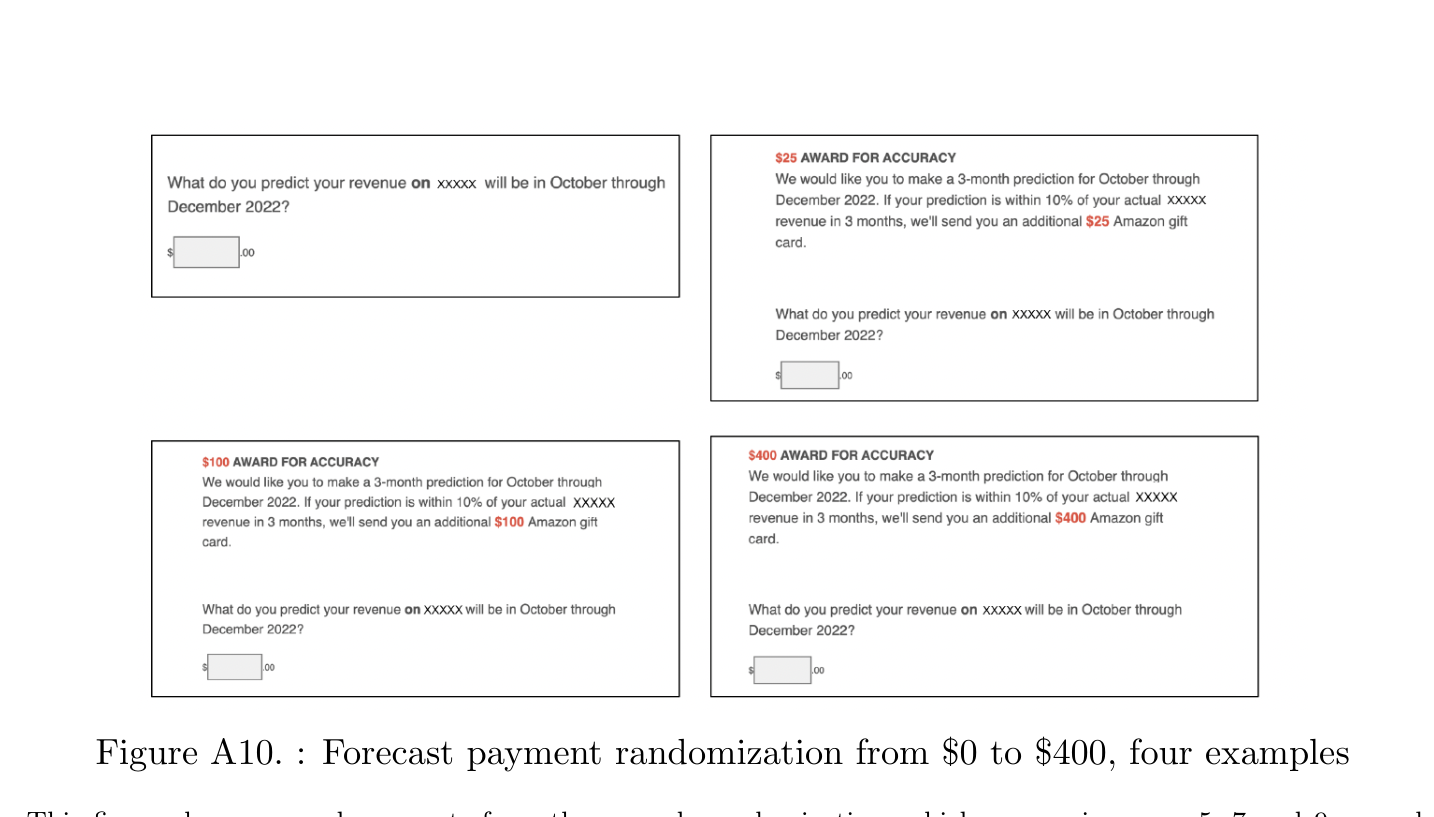

Bloom, Codreanu & Fletcher (2025) elicit incentivized 3-month sales forecasts on a payment-processor platform with the question "What do you predict your revenue on [platform] will be in [month] through [month] [year]?" paired with an accuracy bonus ("If your prediction is within 10% of your actual revenue in 3 months, we'll send you an additional [reward]"). We adopt this wholesale, calibrated to local incomes in CFA, and verify against the merchant's actual Wave activity in the window. Headline expectation: Bloom finds only 18% of US firms land within ±10% of actuals, mean over-optimism of +16% — for SSA mobile-money merchants we expect at least as much.

We pair this with a one-question elicitation of expected non-Wave sales over the same horizon. Most merchants accept some payments off-platform; without the off-Wave share we can't tell whether a low Wave-revenue forecast reflects pessimism or substitution, and we can't calibrate the off-platform-diversion margin that Russel, Shi & Clarke (2025) document for South African revenue-based financing.

images/bloom_forecast_survey.png

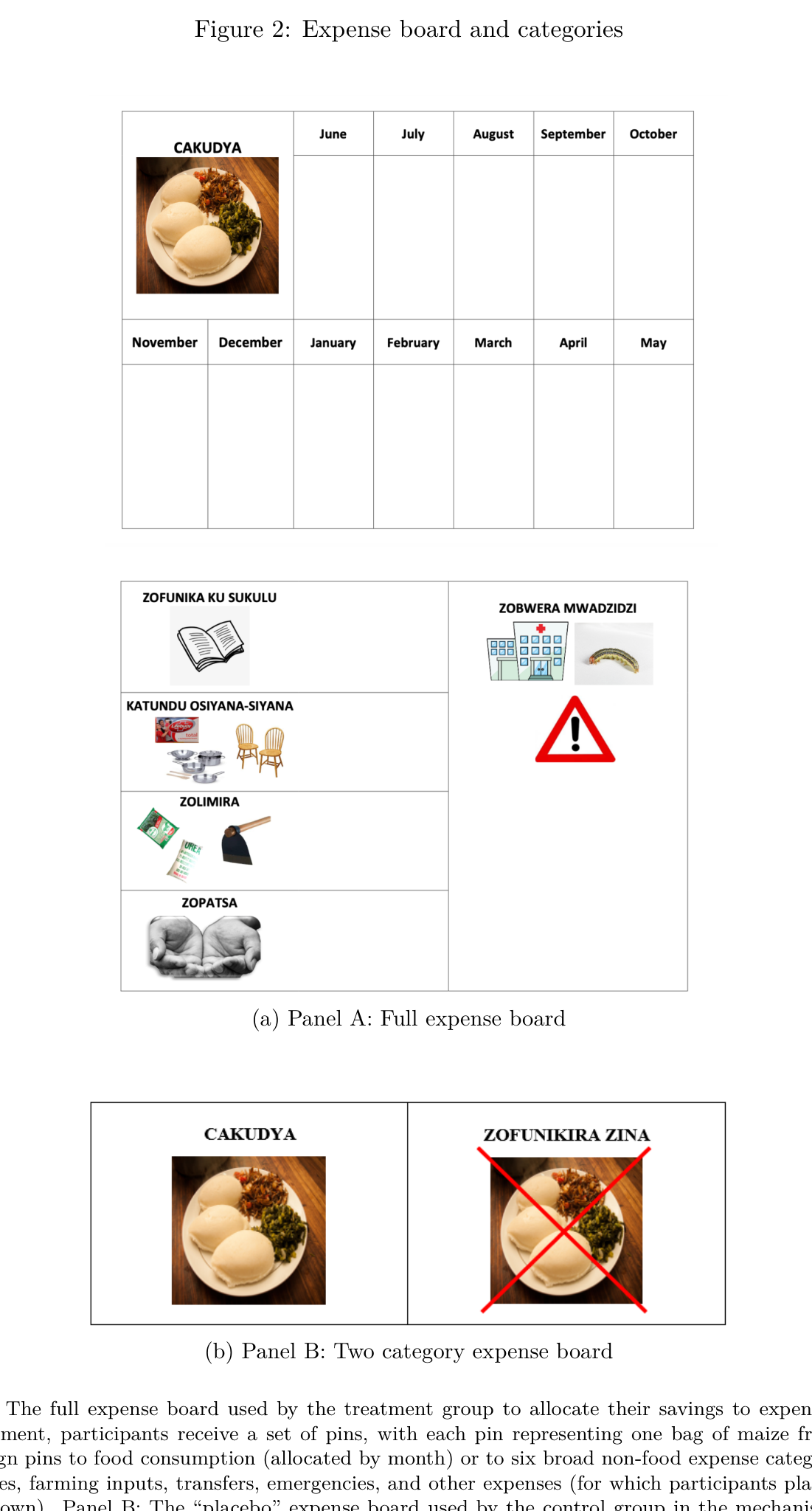

An Augenblick-style expense board, because expenses are the harder forecast

Augenblick et al. (2025) shows that category-cued retrieval — allocating expenses across pre-specified categories — moves beliefs about non-food expenses by 42–62%, raises savings 15–20% months later, and raises crop revenue 8.9% the following year. Bloom's paper suggests that revenue forecasts respond modestly to dashboard exposure; Augenblick's suggests expense forecasts respond a lot when category structure is imposed. We elicit both. If you only had budget to elicit one, the answer is expenses.

images/augenblick_expense_board.png

A Wave-specific fee-belief elicitation — the operationalization of Colin's hypothesis

The same module asks each merchant: "In the past 30 days, how much do you think you paid in fees to Wave?" We verify against Wave's records. The current pricing — 1% on payment volume above 20,000 F/day — means most small merchants pay very little, but the prediction is that they think they pay much more. A measured gap between perceived and actual fees is a directly actionable input for Wave's product communication and for any Chiffres fee-surface decision. The dashboard RCT in §05 then provides the causal complement: a fee-display sub-arm cross-randomized inside the 2×2 identifies whether surfacing accurate fees moves volume.

Three additional belief items that de-risk the cash-advance experiment

Three short items added to the same 3–5 minute module. Each maps directly onto a cash-advance design dimension in §03.

- Gross-margin estimate. One-question elicitation of the merchant's average margin on goods sold. Lets us check whether a uniform 10% deduction rate is systematically more burdensome in low-margin sectors — i.e., whether deduction-rate heterogeneity by sector is worth testing in the cash-advance trial.

- Counterfactual cash-advance use-case and expected incremental return. "If you received an advance of X F today, what would you spend it on, and how much additional revenue, profit, and Wave volume would you expect over the next three months?" Merchants who expect low incremental returns are servicing the deduction out of existing sales rather than new sales — a different selection question for Wave than for merchants who expect the capital to grow the business.

- Stated valuation of sticky platform features. What would the merchant pay for bundled inventory tracking, cash-flow forecasting, or sales-by-category reporting if it came with the cash-advance offer? Operationalizes Russel, Shi & Clarke (2025)'s observational finding that add-on usage cuts the platform-revenue gap 43%, and gives Wave a willingness-to-pay number for the bundle question.

Augenblick et al. (2025) explicitly flag in footnote 1 that expense forecasting is the harder task even in highly volatile-income settings: "This is likely to be true even in low-income settings, where income is highly volatile. For example, while a vegetable vendor's income may fluctuate day to day, the sheer array of certain and uncertain expenses will likely be larger and more volatile." Wave merchants look a lot like the vegetable vendor: many small, frequent inflows; a longer, lumpier list of certain and uncertain outflows (inventory restocks, supplier payments, family transfers, rent, Wave fees, mobile-data, school fees). We expect baseline expense miscalibration to be larger than baseline revenue miscalibration.

The consumer-side Trends ("Dépenses") already surfaces outflows by category — Transferts, Factures, Crédit, Transport, Alimentation, Achats, Santé, Jeux d'argent. Business-side Chiffres today surfaces only inflows (Volume) and fees. A design question for Wave: should the business-side rollout mirror the consumer side and add an outflows / expenses surface? The Phase 1 expense-belief item gives a direct read on the marginal value of doing so without requiring an RCT.

Server-side (Wave admin data, free): Chiffres engagement (views, time-on-page, return visits, category-tab vs. summary-tab visits per Bar-Gill 2024); cash-advance take-up + repayment; transaction count and volume; actual fees paid; voluntary opt-out / category-hide usage (the gambling-transactions concern Colin flagged); continued-use indicator.

Belief module (3–5 minute survey, treatment and control): next-month Wave revenue forecast with accuracy bonus; expected non-Wave revenue over the same window; one expense-category forecast (alimentation / transport / family transfers); perceived fees paid last month; self-assessed forecast win probability (per Bloom — diagnostic of overconfidence); gross-margin estimate; counterfactual cash-advance use-case + expected incremental return; stated valuation of bundled platform features (inventory / cash-flow / category-reporting); short stress / financial-worry module (welfare guardrail).

Endline survey (one round): whether the merchant has hidden any transaction category in Chiffres and which one (welfare / privacy guardrail — consumer-side users have asked support to hide gambling transactions); merchant self-report on whether Chiffres changed any business decision in the past month (free-text plus closed-form on the cash-advance request margin).

Phase 2 · Cash-advance design ¶

─── six product variations · each justified by a belief pattern Phase 1 will identify

Wave's cash advance today. 10% deduction from each incoming customer payment until the advance plus a 10% flat fee is fully repaid. No compounding interest, no late fees, recovery action only when a merchant appears to be deliberately reducing Wave volume to avoid the deduction. Because repayment scales with revenue, the merchant's own expectations — about future Wave revenue, off-Wave revenue, expenses, and fees — are the central determinant of take-up and of which product terms fit. Six concrete product variations correspond to belief patterns Phase 1 will identify or rule out; the Phase 1 evidence then selects which of these to vary in the Gambia cash-advance trial.

Phase 1 outputs are commercially valuable to Wave independent of Phase 2: a sector-margin slice on deduction burden, the perceived–actual fee gap, willingness-to-pay for bundled platform features. Phase 2 uses those Phase-1 reads to pick which of the six variations above to vary in the Gambia trial — turning Phase 1's measurement into a pre-registered product-design choice rather than an ad-hoc one. The two phases can also run on different markets (Phase 1 across SN / CI / GM, Phase 2 in The Gambia), which keeps identification clean and lets each phase report on its own timeline.

The evidence base ¶

─── seven papers anchor what we expect

The full tight lit review is at wave-trends.pages.dev → Bibliography with structured summaries for 33 papers. The seven that anchor the pitch:

- Bloom, Codreanu & Fletcher (2025), Rationalizing Firm Forecasts. Five-year, ten-wave panel of 6,594 US firms on a payment processor; only 18% of forecasts within ±10% of actuals; mean +16% over-optimism; dashboard look-up moves bias contemporaneously without persisting. → measurement template.

- Augenblick, Jack, Kaur, Masiye & Swanson (2025), Retrieval Failures and Consumption Smoothing. Zambian farmers; expense board moves non-food forecast 42–62%, savings 15–20%, next-year crop revenue 8.9%. → mechanism for the rules-of-thumb arm.

- Dalton, Pamuk, Ramrattan, van Soest & Uras (2024), Electronic Payment Technology and Business Finance, MS 70(4). Kenyan SMEs on Safaricom's merchant product; +50% mobile-loan access, zero on revenue/profit, reduced volatility for small firms. → closest direct precedent.

- Bar-Gill, Brynjolfsson & Hak (2024), Helping Small Businesses Become More Data-Driven, MS / NBER WP 31089. eBay Seller Hub rollout; +3.6% sales ITT, >1/3 monitoring-mediated. → upper-bound dashboard analog.

- Gertler, Higgins, Malmendier & Ojeda (2025), NBER WP 33387 (R&R Econometrica). 33,978 Mexican Clip merchants; reminders +15%, pre-announced reminders +7.8% more; trust-mechanism concentrated in newer-relationship merchants. → direct precedent for Wave's T1 arm and the pre-announced-push sub-arm.

- Russel, Shi & Clarke (2025), Revenue-Based Financing, HBS WP. 100M+ transactions, 250K South African businesses; advance-takers process 16% less on-platform revenue eight months later (≈60% adverse selection, ≈40% moral hazard via off-platform shifting); bundled add-on features cut the gap by 43%; six-month screening windows beat three-month by 5% on post-advance revenue. → closest LMIC evidence on cash-advance frictions and screening; informs the Gambia cash-advance pilot, not the Trends design.

- Cordaro, Fafchamps, Mayer, Meki, Quinn & Roll (2025), Finance and Mutuality, WP. Field experiment in a Kenyan multinational's supply chain (FoodCo); a hybrid contract (income-share capped at debt-equivalent total) raises distributor monthly profits 170% ITT vs. control vs. 59% for standard debt at identical take-up, with higher repayment and higher business-practice scores. → performance-contingent contracts with high-frequency observability can dominate fixed-payment debt; supports the structural choice behind Wave's deduction-based cash advance.

Phase 3 (optional) · A dashboard RCT timed to the business-Trends rollout ¶

─── 2×2 engagement × content · no-contact control · fee-display sub-arm

The Phase 1 measurement and the Phase 2 cash-advance trial stand on their own without Phase 3. We include Phase 3 here because the business-Trends rollout itself is a natural setting for a causally-identified test of dashboard design — whether category-broken-down Chiffres moves merchant forecast calibration, business practices, and downstream revenue; whether engagement nudges sustain that effect after removal; whether surfacing fees moves volume. This would be the published dashboard paper from the collaboration. Wave's commitment in Phase 3 is larger than in Phase 1 or 2, and Phase 3 only makes sense in coordination with the SN / CI rollout calendar, so we include it as an explicit option rather than a default.

Design

Merchants in the business-Trends rollout are randomly assigned to one of four cells crossing engagement (cold push vs. pre-announced push + login-tied incentive, after Gertler et al. 2025) with content (default Chiffres view — Volume + Frais — vs. category-broken-down Chiffres with personalized rules-of-thumb derived from each merchant's own transaction history), plus a pure no-contact control. A fee-display sub-arm is cross-randomized inside the design to causally identify the fee-perception effect. A per-category opt-out guardrail handles the welfare concern that consumer-side users have asked support to hide gambling transactions from Trends.

images/wave_business_chiffres.png

Default Chiffres

Category + rules of thumb

Cold push

Pre-announced push + login incentive

The engagement arm, by analogy

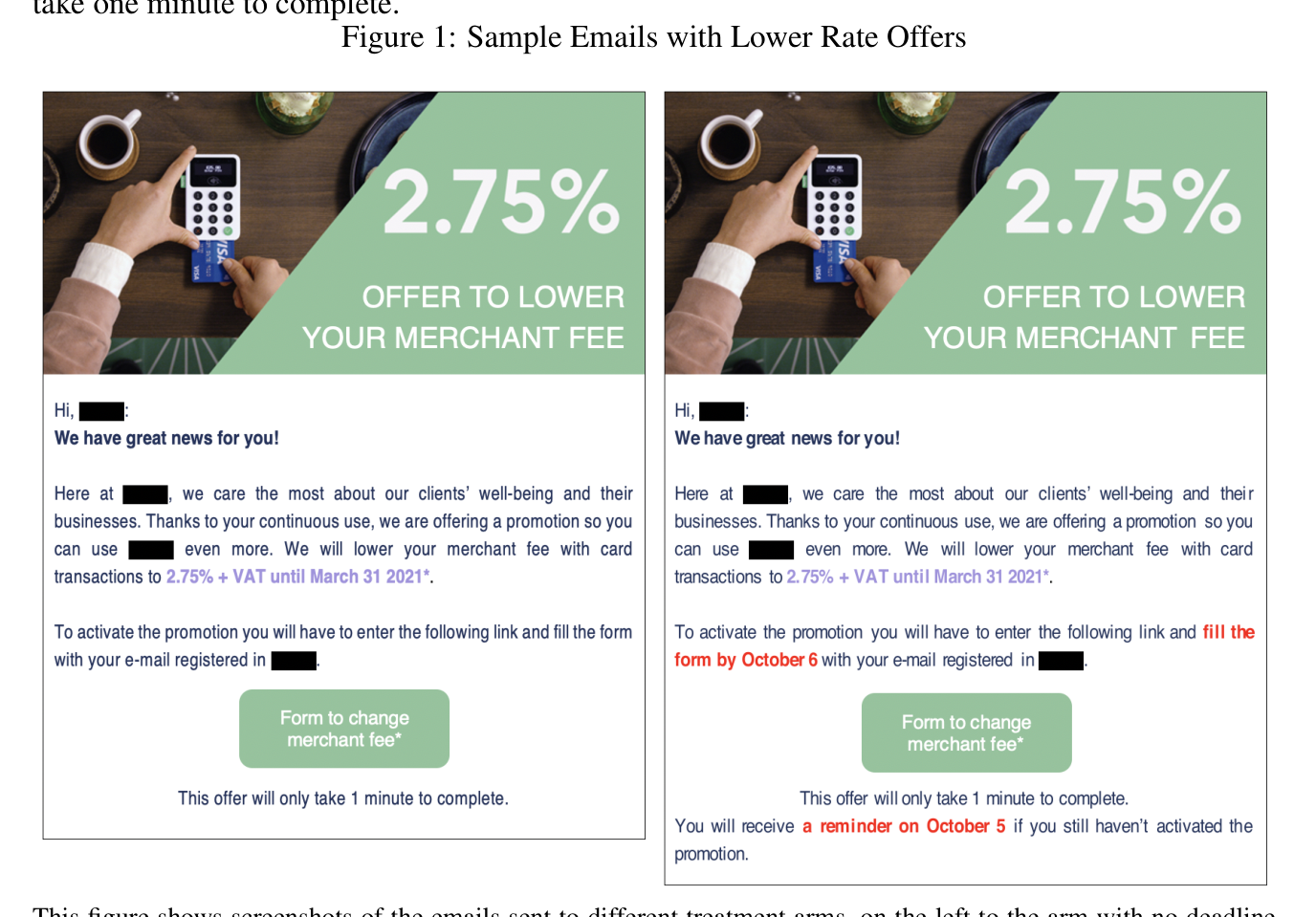

The engagement dimension of the 2×2 is modeled directly on Gertler et al. (2025), who ran a large field experiment with 33,978 Mexican Clip merchants — small retailers on a payments platform structurally similar to Wave's merchant base. Clip cross-randomized fee discounts, plain reminders, pre-announced reminders, and deadlines. Reminders raised adoption by 15%; pre-announced reminders raised it by an additional 7.8 percentage points on top of plain reminders, with the effect concentrated in newer-relationship and lower-trust merchants. The mechanism is trust-building: telling a merchant "you will receive a reminder on October 5" and then actually doing so demonstrates platform reliability in a way a cold push cannot. Wave's situation in SN / CI maps closely — business merchants are newer to Wave than consumer-side users, the trust mechanism should be at least as strong, and the channel (in-app push + login-tied incentive) is directly available.

images/gertler_clip_email.png

Cross-randomized sub-arms (orthogonal to the 2×2)

Fee display. Half of treated merchants receive a "fees-this-month" line surfaced prominently on the Chiffres summary; the other half do not. This is the operationalization of the fee-perception measurement from Phase 1 — Phase 1 measures the perceived-vs-actual fee gap; this sub-arm causally identifies whether surfacing accurate fees in Chiffres changes the volume that merchants accept through Wave. Orthogonal randomization inside the 2×2 cells lets us identify the fee-display effect within both content conditions.

Per-category opt-out (welfare guardrail). Consumer-side Trends users have explicitly asked support to hide gambling transactions. The business-side experiment defaults to showing per-category hide controls in all treated arms and pre-registers the rate of voluntary hiding (by category) as a primary welfare outcome. No moralizing language appears in any rules-of-thumb copy — only fee and revenue framings, no spending-discipline framings on gambling-like categories.

Manual entry of non-Wave revenue (optional, smaller). A subset of merchants in the category-breakdown arms get a way to log non-Wave revenue (cash, alternative channels) inside Chiffres. This tests whether fuller category information amplifies the dashboard effect, and whether Wave's underwriting against a fuller revenue picture is more predictive of cash-advance repayment than Wave-only data — directly informative for Phase 2's loan-size formula.

Timeline

Sample size

Five arms × ~2,500–3,500 merchants per arm ≈ 12,500–17,500 merchants total. This is in the same order of magnitude as Gertler et al. (2025) Clip Mexico (n = 33,978) and well above Dalton et al. (2024) Kenyan SMEs (n = 620). It supports detecting engagement effects of 3–5 percentage points and forecast-calibration effects of 0.1 SD with adequate power. We can run smaller and accept wider confidence intervals; the order of magnitude is what we would defend in a pre-analysis plan. The design read at month 3 (above) feeds into Phase 2 cash-advance variation selection — Phase 2 does not have to wait for the persistence read at month 12+.